Private equity has been slowly creeping into Ethiopia since Schulze Global first set up shop here in 2008. But the pace of entry is about to pick up dramatically.

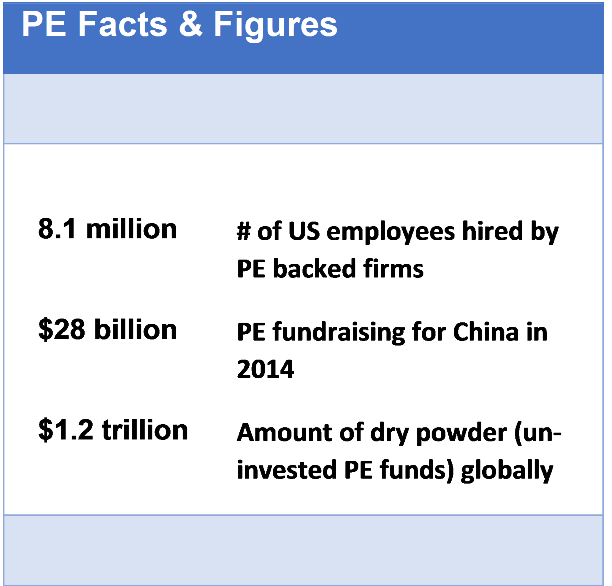

With $1.2 trillion worth of un-invested funds globally, private equity (PE) – a form of investment involving the purchase of a portion or all of a privately held company’s shares – is one of the more consequential investment asset classes in the world today. Although most PE investments occur in the US (where PE backed firms account for over 8 million jobs), their increasingly global reach is holding out hope that similar benefits may be in store for the African continent and indeed in Ethiopia as well even if it is clearly still in its infancy here.

There are an increasing number of PE firms looking to engage here but the number of them resident in Ethiopia, you can still count on the fingers of one hand. Since Schulze Global Investments (SGI) became the first such foreign firm to set up shop in 2008, there has hardly been a flood of new entrants following in its footsteps although there have been more transactions than most people might think. It looks like that could change in the near future according to sentiment from the recently concluded World Economic Forum on Africa in Cape Town. According to a survey of executives from major international firms at the summit, Ethiopia has now supplanted Nigeria as the African market with the strongest growth building on recent trends showing the number of FDI projects in Ethiopia surged 88% in 2014 year over year while Nigeria showed a growth rate of just 17%. Considering that private equity investment in Sub Saharan Africa (SSA) had in years prior shifted significantly away from South Africa towards Nigeria (investing just under $1 billion there in the first 6 months of 2014), it appears that a similar shift to Ethiopia may be on the horizon.

Coming to Africa

The growth of private equity in Africa has mirrored growing consensus that the continent and its frontier markets are the new engines of global economic growth. Starting from a small and narrow base totaling just $300 million in 2002 (mostly directed towards South Africa), transactions peaked at $8.3 billion in 2007. Subsequent to the recovery from the financial crisis of 2008, they have been growing steadily since 2010, reaching $8.1 billion in 2014 (AVCA). Sub Saharan Africa in particular has been outperforming other emerging markets with regards to increased inflow of private equity investment showing an increase in 2014 of 13% year-over-year while others all declined compared with 2013 (EMPEA).

| Selected Reading on PE in Africa |

|---|

| Into Africa: The Rise of Private Equity (Freshfields Bruckhaus Derringer) |

| Game on: Private Equity Investment in Africa (PWC) |

| Towards a Framework for Attracting Venture Capital and Private Equity in Ethiopia (UNDP) |

| The Case for Country Specialization (SGI) |

| Private equity in Africa: Context, opportunities, and risks (Allen & Overy) |

| Private equity in Africa Issues Paper (UNECA) |

There are fundamental drivers to the shift of private equity towards Africa and SSA in particular. While markets may not be as large as those found in developed economies, in many countries on the continent, they are growing at a far faster rate with correspondingly more attractive ROIs. Furthermore, otherwise limited access to finance for most businesses mean that equity investment in them can usually be achieved with very attractive entry valuations. Management capacity is generally another limiting factor for such businesses that can also be addressed to great effect by private equity firms. Finally, the relatively underdeveloped nature of many African economies means that the competitive environment is not as prohibitive as in more developed markets.

This combination of attractive pre-money valuation, enormous headroom for growth and a comparatively less competitive environment in which to recognize it, is exactly why private equity investment in Africa is increasing faster than anywhere else in the world. Moreover, the reasons underpinning this growth are fundamental in nature implying that the current trajectory is likely to continue in the near to mid term at the very least.

The nature of private equity investment in Africa has also seen major changes in the last few years. Chief amongst these is the shift of focus away from South Africa to East and West Africa with Nigeria having been a clear beneficiary until the recent drop in global oil prices. Much bigger firms are also buying into the African growth story bringing with them correspondingly larger transactions.

Private equity’s entry into Ethiopia has been a bit more hesitant than in the rest of Africa. In fact, SGI was the only country specific fund until recently when the likes of Renew Strategies, Verdant Frontiers (both of which are not quite the typical PE) and Ascent Capital joined the mix in the past few years. There have, however been at least 31 transactions by 15 firms with several more pending in 2015. The lack of familiarity with this type of investment has contributed in some measure to its somewhat halting acceptance in Ethiopia. Furthermore, as is the case in much of Africa, many businesses here tend to have family owned origins with proprietors who are reluctant to give up ownership stakes. Although the regulatory framework might not necessarily be optimal for this type of investment, neither does it pose prohibitive challenges as the existing number of transactions attest to. Many of these challenges look set to ease over the near term as they indeed should, given what private equity can do for the nation’s private sector and economic development.

Private Equity Transactions in Ethiopia

| PE Firm | Investee | Sector | Year |

|---|---|---|---|

| 8 Miles | Awash Winery | FMCG - Beverages | 2013 |

| 8 Miles | elleni LLC | Agri & Fin Services | 2013 |

| African Wildlife Capital | Limalimo Lodge | Tourism | 2014 |

| Arabica | Mekelle Farms | Agriculture | 2014 |

| Arabica | Belcash | Technology | 2014 |

| Ascent | International Clinical Laboratories | Medical Services | 2015 |

| Bluebird Holdings | Green PLC | FMCG & Chemical | |

| Catalyst Principal Partners | Yes Water | FMCG - Beverages | 2013 |

| Duet/Vasari | Dashen Brewery | FMCG - Beverages | 2012 |

| Vasari | Rorank Business PLC | FMCG - Beverages | 2015 |

| Fairfax Africa Fund | Ethiopia Crown& Cork | Manufacturing | 2015 |

| KKR | AfriRose | Floriculture | 2014 |

| Qalaa Holdings | Ascom Mining | Mining | 2014 |

| Renew | dVentus | Energy | 2013 |

| Renew | Mama Fresh | FMCG - Food | 2014 |

| Renew | Metad | Coffee | 2013 |

| Renew | East Africa Emergency Services Ltd | Medical/Education | 2015 |

| Roha Ventures | Juniper Glass | Industry | 2014 |

| Schulze Global Investments | Jalannera Coffee | Coffee | 2012 |

| Schulze Global Investments | Flipper International School | Education | 2012 |

| Schulze Global Investments | Kaliti Food S.C. | FMCG - Food | 2013 |

| Schulze Global Investments | Sa-Med | Medical Equip Mfg | |

| Schulze Global Investments | National Cement S.C. | Manufacturing | 2012 |

| Schulze Global Investments | Southwest Energy | Energy | 2012 |

| Silk Invest | NAS Foods | FMCG - Food | 2012 |

| Surya | Cambridge Industries | Energy | 2012 |

| Vasari | Ahadukes Food Products | FMCG - Food | 2013 |

| Verdant Frontiers | ET Constr Equip Rentals PLC | Leasing | 2013 |

| Verdant Frontiers | Wudassie Diagnostic Center | Medical Services | 2013 |

| Verdant Frontiers | Verde Beef Processing | Agriculture | 2014 |

| Verdant Frontiers | Omo Valley Lodge | Hospitality | 2015 |

| Bluebird Holdings | Health Care Food Manufacturers PLC | FMCG | |

| Bluebird Holdings | Gulele Soap Factory | ||

| 54 Capital | Aquasafe |

The PE Advantage

There are a number of reasons why private equity represents an attractive alternative to debt and other forms of investment from a developmental perspective. Its focus on investing in existing businesses, growing them and then exiting, is by its very nature a suitable vehicle for knowledge transfer to a domestic private sector sorely in need of it. It is also much more vested in the success of the investment than something like a bank would be since its success is directly linked to that of its investments in a way that generally outperforms its industry peers. Consequently PE firms will generally spend a lot of time and effort in equipping themselves with the best possible business intelligence in order to maximize their prospective investment’s ROI. Finally, they bring with them management expertise including institutionalized governance models, proven operational frameworks and best practices as well as market and supply linkages that can sometimes be as valuable to the recipient company than the attendant infusion of capital.

Capital, is of course the biggest need facing businesses looking to grow, primarily due to the dominance of the public sector in claiming the lion’s share of available funds (domestic credit to the private sector is 12.6% of GDP as of Q1 2014/2015 compared to a regional average of 29.3% for SSA, WorldBank). The myriad infrastructure projects which are the building blocks of Ethiopia’s growing economy demand such spending from the public sector but without the financing to support it, the private sector is unable to fully take advantage of this growing infrastructure, leaving potential gains for the economy, unrealized.

Growth capital then, is a potentially critical catalyst in helping propel the indigenous private sector evolve and that is generally what private equity players in Africa bring. Furthermore, they do so in foreign exchange, the shortage of which is yet another severe constraint faced by many Ethiopian businesses for both capital and operational expenditures. Taken together – access to finance, limited management capacity and shortage of forex account for a very sizable portion of the challenges most businesses in Ethiopia must overcome in order to scale in a way that meets the new demands of a rapidly transforming economy.

Growth capital then, is a potentially critical catalyst in helping propel the indigenous private sector evolve and that is generally what private equity players in Africa bring. Furthermore, they do so in foreign exchange, the shortage of which is yet another severe constraint faced by many Ethiopian businesses for both capital and operational expenditures. Taken together – access to finance, limited management capacity and shortage of forex account for a very sizable portion of the challenges most businesses in Ethiopia must overcome in order to scale in a way that meets the new demands of a rapidly transforming economy.

From a government perspective, this type of investment certainly should tick many of the boxes that might be of concern – institutional governance models which generally favor strict compliance with regulations (tax or otherwise), provides financing to the private sector without ‘impacting’ what the public sector needs, all while ensuring domestic capacity is upgraded and retained in country indefinitely.

There is one significant component of potential growth in Ethiopian business that typical private equity won’t address. A category of business (or financing for it) known as the Missing Middle – businesses too big for schemes like microcredit but too small for institutional investors. In fact this is one of the factors that may well prove to be a constraining factor for the growth of private equity in Ethiopia over the long term.

Even in this particular scenario though, investment firms such as Renew Strategies and Verdant Frontiers are notable exceptions since they operate with lower investment thresholds (Renew) or are directly engaged in business incubation activities (Verdant). Not only do such activities tap into an even greater reservoir of potential growth, they can also create a feeder system for the more traditional private equity firms trying to source deals.

Challenges in Ethiopia

There are a number of areas in which PE firms seeking to do deals in Ethiopia currently face challenges. An ambiguous regulatory context, weak business environment, limited exit options and income repatriation encompass the majority of these. However, none of them are insurmountable and in fact those firms which have already executed transactions here, have found a variety of ways to overcome many of them.

The numerous restrictions on foreign investment in everything from consulting to retail are likely to be amongst the first and lasting challenges that private equity firms will face in Ethiopia. Even to the extent of some ambiguity on how one can set up shop in Ethiopia should there be a desire to do so although it is not absolutely necessary. Special purpose vehicles through which to execute transactions will also face similar challenges and will likely need to be established off shore if needed. Although policy makers have apparently undertaken early efforts to understand and resolve regulatory issues that private equity firms might face, a timeframe in which this might materialize, has not yet been announced. In the meantime, linking up with a local partner that can undertake the required activities on behalf of an offshore entity can solve most of attendant problems and is probably advisable anyway in order to help navigate through Ethiopia’s unique business environment.

Perhaps a greater impediment to the adoption of private equity at a larger scale than seen today, is the scarcity of investment targets that meet requirements for size, management capacity and organizational structure that PEs usually look for. The relatively weak and uncompetitive business environment in Ethiopia combined with the paucity of credit means that most Ethiopian businesses are simply not at the stage of development where the institutional criteria implicit to most PE funds can be met. For example, amongst these criteria are usually investment size which is likely to be USD $5 million or more, far greater than what many companies would be able to efficiently absorb. The increasing number of new entrants into the Ethiopian private equity scene will therefore up the competition for deal flow and perhaps become a sizable constraint on its growth in the next 3-5 years.

Limited management capacity and corporate governance models at most Ethiopian companies means that due diligence is also a challenging area. Implementation of IFRS accounting standards for example, is a rarity although pending regulation requiring this of most businesses could ease this problem going forward. In any case, much of this due diligence is usually outsourced to domestic companies or international consulting companies with local presence (such as Ernst & Young, DeLoitte, etc.) and while they will generally be well versed with local practices, it will take correspondingly more time and effort to complete.

Finding the human capital needed to take Ethiopian businesses to the next level won’t be easy. CFOs and COOs are a particularly rare commodity that PE firms might ordinarily like to focus on bringing aboard quickly. The availability of companies which can implement ERP systems (another favorite tactical upgrade of PE firms) has been low in the past but is improving quickly.

It is of course no surprise that exiting investments here (as it is in most places on the continent) is more of a challenge than it is in countries that have sufficiently capitalized securities markets. Therefore investors testing the waters will already be cognizant and prepared for exit strategies that do not rely much on IPOs. Given the relatively recent appearance of this asset class in Ethiopia (with investment horizons that are typically 5-10 years in length), there are not many examples that we can cite in terms of exits. It would therefore appear that sales to strategic investors (such as MNOs) or other PE firms is the most likely exit route to be taken in the near term based on the experiences of other countries in SSA thus far.

Closely related to this challenge is that of actually repatriating the profits recognized from the exit (or indeed from dividends that are recognized from operating profits). While there is no legal restriction on doing so (given investments are executed in accordance with the legal requirements thereof), the general scarcity of foreign exchange in an economy which routinely carries a sizable trade deficit, is indeed one of the daunting prospects any foreign investor must face. Particularly so with private equity which must return profits to its limited partners in accordance with the declared intent of the applicable fund(s) it is deploying. However, in the general case even this is not insurmountable and in most cases simply implies delays of a few months rather than any extended difficulty in doing so.

There is the expectation that Ethiopia’s trade deficit will see a gradual improvement as the move towards industrialization picks up steam along with the addition of major exports such as power and sugar. These are pillars of the government’s Growth and Transformation Plan(s) with the latter two especially expected to commence substantively in the next 2-3 years. With regards to the former, despite continued underperformance in both exports and import substitution, there is no doubt that it will have a significant impact on reducing the trade deficit – and by extension chronic forex shortages – over the longer term. Of course the contribution of private equity to enabling such industrialization is another one of the key developmental benefits that make it attractive. Moreover, carefully balanced portfolios that include as a major component, businesses that earn foreign currency, can also help to directly address income repatriation challenges for their operators since some portion of forex earnings can be used by a given company to address its own operational needs in addition to profit withdrawals. When it comes to exits, should the buyer be based abroad, it is possible for the transaction to be executed offshore and in foreign currency making the prospect of repatriating profits, a moot point.

Of course these are challenges specific to this type of investment vehicle and others remain that are generally shared across the wider business community. As such, all investors would be well served to understand Ethiopia’s unique regulatory, cultural and business environment attributes in order to overcome the implicit challenges within them as well as capitalize on the attendant opportunities.

Preparing for Lift Off

Many of the preconditions necessary to make Ethiopia an increasingly attractive destination for global PE investments, are already present. And given the possibility for this type of investment’s contribution to growth and development, an enabling regulatory environment should be a focus of policymakers sooner rather than later. A UNECA report on the topic recently stated of private equity that it can be, “…a catalyst and accelerator for growth, provided that there is already significant positive economic momentum.”

This is exactly what is present here in Ethiopia today and policymakers should therefore develop a deeper understanding of private equity in general, how it is manifesting itself currently in Ethiopia and the challenges in front of it that should be addressed in order to increase its developmental impact dramatically.

Notable amongst the challenges that are already in the process of being addressed are the impending creation of a legal framework for holding companies and the adoption of IFRS as a mandatory accounting standard for business. Both of those will yet take some time to materialize but at least they are in process. With regards to opening up additional areas for foreign investment, it is less certain what might be on the horizon. But there should at minimum be consideration for opening up some currently restricted areas outright (such as in consulting) and at least a gradual easing (by allowing joint ventures) in others.

The private sector needs to understand that competitiveness in the Ethiopian environment is going to move steadily upwards due to the influx of cash and management expertise that FDI will increasingly bring. Every business must therefore either prepare to elevate its own ability to compete in such an environment organically or make itself an attractive target for investment. Developing an understanding of private equity, improving management capacity, implementing recognized corporate governance models (such as King III) and adopting IFRS accounting standards are some of the ways this could be done.

Overall, the slightly longer term challenges which private equity in Ethiopia will face with regards to sufficient deal flow, ought to be addressed in partnership between the public and private sectors. While it’s true that there are a variety of efforts to improve the capacity of small and micro enterprises (such as via UNDP’s Entrepreneurship Development Programme and DFID’s Private Enterprise Programme Ethiopia), their alignment with the particular needs of private equity is uncertain. Government policy too places a great deal of focus in fostering the creation of such businesses. It should therefore be a logical next step to marry up the various resources working in this space to create a somewhat structured pipeline that can help elevate the smaller, home grown businesses to the kind of size and operating modalities that can allow them to be attractive investment targets should their proprietors desire it. Even if they don’t, their ability to compete in a business landscape that could see enormous transformation in the near to mid term, will be beneficial not only to them but to the larger economy as well.

Editor’s note: Ethiopian Business Review has previously published an edited and summarized version of this article in its Sept/Oct, 2015 issue.

Leave a Reply